Why Target Date Funds Are the Best Companion to VT

Why TDFs in tax-advantaged accounts are perfect for 99% of Americans

I consider the Vanguard Total World Stock ETF (VT) to be the GOAT innovation in retail investing.

✅ Nearly 10K stocks tracking global markets

✅ Extremely cheap (0.06% expense ratio)

✅ Completely hands-off

For retail investors, VT is the only investment product you ever need in a taxable brokerage account. But a complete investment portfolio needs bonds—and that’s where the second greatest innovation comes in: Target Date Funds (TDFs).

TDFs are simple, one-fund solutions helping you save for retirement.

Stocks & Bonds: Why Both Matter

A strong portfolio balances stocks for growth and bonds for stability.

📈 Stocks = Growth → Stocks represent ownership in companies and drive a portfolio’s long-term returns.¹ They are higher risk, and therefore, generate higher returns. When you’re young, time is on your side, so you can take on more risk.

📉 Bonds = Stability → Bonds represent debt obligations and provide stability, especially as you near retirement. Bonds are lower risk compared to equities, and therefore, generate lower returns. When you’re older, you’re closer to retirement, so you have to take on less risk.

But there’s one key issue: bonds distribute income regularly, which makes them inefficient in taxable accounts. Remember, Uncle Sam hits taxable accounts twice:

You’ve already paid taxes on money going in.

You pay taxes again on dividends, interest, and capital gains.

And so, because bonds distribute income regularly, they belong in tax-advantaged accounts.

What’s a Tax-Advantaged Account?

A tax-advantaged account offers benefits either when contributing (i.e., deferring taxes now and paying them later) or withdrawing (i.e., paying taxes today for lifelong tax-free growth):

📌 Common tax-advantaged accounts:

Roth & Traditional IRAs

Roth & Traditional 401(k)s

HSAs (Health Savings Accounts)

Unlike taxable accounts, there are no taxes on buying or selling investments within these accounts—tax rules only apply when withdrawing.

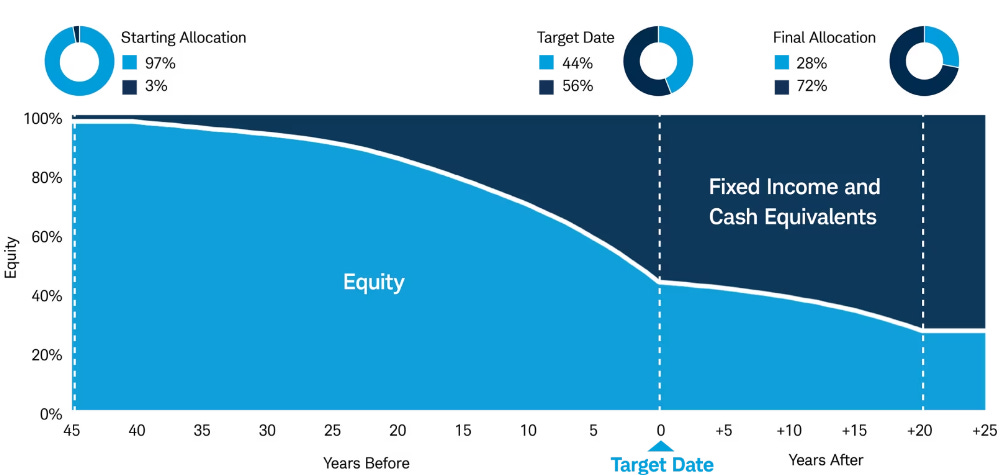

Why a Target Date Fund (TDF)?

TDFs automatically balance stocks & bonds for you.

✅ Diversified stocks (U.S. & international, like VT)

✅ Bonds added gradually as you age

✅ Automatically rebalances over time

This is called a “glide path”—the fund sells stocks and buys bonds as you near retirement.

💡 The biggest advantage? It removes the psychology of investing. You don’t need to manually rebalance or second-guess yourself. Just set it and forget it.

What Target Date Funds Should You Buy?

Not all TDFs are created equal.

Some funds are packed with high fees. You want a TDF built with low-cost index funds—aim for expense ratios under 0.25%.

Here are a few examples of the best low-cost Target Date Funds:

Schwab Target Index Funds (0.08%)

Fidelity Freedom Index Funds (0.12%)

Vanguard Target Retirement Funds (0.08%)

My portfolio?

Taxable account (at Fidelity): 100% VT²

Roth IRA (at Schwab): 100% SWYNX

Trad. 401K (at Fidelity): 100% FFLEX

HSA (at Fidelity): 100% FFLEX

That’s it. It really is that simple.

¹ Stocks return more than bonds because investors demand compensation for taking on higher risk—this is known as the equity risk premium. Over long periods, equities outperform because they are more volatile, but that extra risk comes with higher expected returns.

² I also hold some low-cost index funds, including SCHB, VEA, and VWO, from my days as a Wealthfront user, which I’ve kept to avoid triggering taxable events. Since 2021, all new investments have gone into VT.